FDIC-Insured - Backed by the full faith and credit of the U.S. Government

-

-

-

FNBO

Mortgage

Date Published: December 23, 2021

-

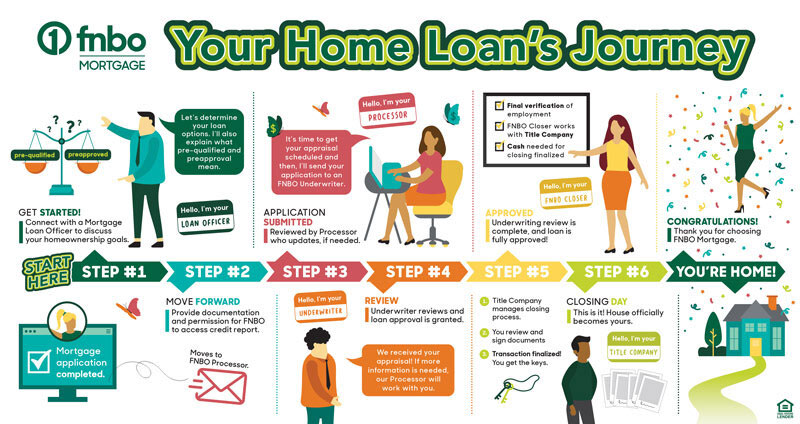

The Journey of a Home Loan – Application to Closing

If you’re a potential homebuyer and you’re thinking about jumping into the market, this probably means that you will need a mortgage loan. Eighty-seven percent of homebuyers do, so you’ll be glad to know that, with a little context and the support of a loan officer, the process is fairly easy to navigate.

To help you on your way, we’ve outlined the journey of a mortgage loan below. This easy-to-follow- guide outlines the path of a typical home loan and preapproval process. Our goal is to help you understand the steps that are required when you purchase your first or next home.

- Getting Started on the Home Loan Journey

The mortgage process starts, simply enough, with identifying a loan officer. This mortgage lending professional will be there to guide you throughout your journey and will start by helping you to gain a preapproval, or a pre-qualification, and they will explain the difference.

Unlike a pre-qualification, where an estimate is provided for how much home you can afford, a preapproval takes it a step further and determines the amount you are eligible to borrow. This is accomplished by taking a deeper look at your financial position and goals.

The preapproval process is in place to more accurately ensure that you will ultimately be approved for your home loan. Since most sellers prefer to accept offers from a buyer who is preapproved, this is a critical step you should undertake before you start your home search, especially when the housing market is competitive.

One of the first steps in the preapproval process is to provide a two-year living and working history as well as to grant permission to your lender to access your credit report. A thorough review of your credit history, including a check of your credit score, is essential when it comes to determining how much you’ll need to put down on your purchase as well as the interest rate for which you may qualify. Information obtained through a credit report may also have bearing on the type of loan you should consider. Good thing your trusty loan officer is by your side!

Your loan officer will also discuss your mortgage options with you and determine which type of loan best suits your needs. Fixed or adjustable, Conventional or FHA? There are a lot of options, and your loan officer will be a valuable resource when it comes providing all of them and helping you make the best decision for the next course of action.

- Moving Forward on Your Loan Application

Once you’ve made an offer on a home, and it’s accepted, you’ll need to officially apply for financing. In addition to filling out and submitting the application during the preapproval process, you’ll now be asked to provide certain documentation, such as paystubs, tax documents and bank statements to name a few.

Once all documentation is submitted, your application moves to a loan processor. It is the processor’s job to review each document and ensure that all of the pieces are in place. If necessary, the processor may request additional information to ensure that your loan is ready for the next step on its journey.

- Ordering the Home Appraisal

Once the processor verifies the information you have provided, he or she will order a home appraisal, an estimation of the value of the property you intend to buy. A licensed appraiser will conduct an on-site review and compare your purchase to others in the neighborhood (comps). The goal is to ensure that the price you agreed to pay is not overinflated, requiring you to spend more than the property is worth.

Then, with all documentation submitted and verified, and a home appraisal completed, your application is ready to move to the next phase of its journey when it is received by an underwriter.

- Reviewing Your Loan Application

The underwriting process may be one of the least understood steps in obtaining a mortgage. Simply put, it’s a last check of the information you have provided and when you receive approval on the final amount of your mortgage loan.

While an underwriter is there to protect the interest of the lending institution, the halo effect protects you, the buyer as well. That’s because an underwriter will verify the information you have submitted by checking data with third-party sources. He or she may also ask for additional documentation. The process has been designed to ensure that you don’t close on a mortgage you can’t afford.

Once the t’s are crossed and i’s are dotted, your underwriter will grant approval for your loan, sending you onward to the next step in your mortgage journey.

- Receiving Your Mortgage Loan Approval

While the underwriting process can be completed in as little as a few days, it typically requires an underwriter just over a week to make the final verifications and provide approval. Of course, your loan may require more time in underwriting depending upon the particulars of your situation, so don’t be alarmed if it takes a little longer.

Once approval is granted, your loan then moves to a closer who makes a final verification of your employment and determines the cash necessary to finalize the closing. At this stage of the process, your closer also begins working with the title company. The title company is responsible for finalizing the purchasing process and facilitating the closing of your loan.

- You’ve Made It—Closing Day Has Arrived!

When closing day arrives, it’s time for your happy dance, because you are only a few steps away from taking ownership of your new home. However, the process really kicks into high gear three days before closing, when you receive disclosures from your lender. It’s essential that you take time to read them and ask any questions you might have before you arrive on closing day.

At your closing, you’ll be asked to sign these documents as well as others related to your mortgage and home purchase. You may feel like you’re adding your John Hancock to the paperwork frequently during the process, but soon, you’ll be handed the keys to your new home. That’s when a fabulous new chapter of your life begins.

As for you loan, its journey isn’t complete, but that’s where you come in: month by month, you’ll nurture your mortgage with payments and watch as your investment blossoms into home equity!

The articles in this blog are for informational purposes only and not intended to provide specific advice or recommendations. When making decisions about your financial situation, consult a financial professional for advice. Articles are not regularly updated, and information may become outdated.

-

Nearly 170 years of putting customers first.

-

-

Products

-

-

-

Company

-

-

-

Legal Information

-

© 2026 First National Bank of Omaha (FNBO). All Rights Reserved. 1601 Dodge Street, Omaha Nebraska, 68197

FNBO is an Equal Opportunity/Affirmative Action/Veterans/Disability Employer.

NMLS 412727

Cards are issued by FNBO (First National Bank of Omaha), pursuant to a license from Visa® U.S.A., Inc. Visa® is a registered trademark of Visa® International Service Association and used under license.

Only deposit products are FDIC insured.

Investment Products are: NOT FDIC INSURED • NOT A DEPOSIT OR OTHER OBLIGATION OF THE BANK • NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY • NOT GUARANTEED BY THE BANK • MAY LOSE VALUE

Awards based on independent surveys and editorial methodologies for the years shown. Recognition does not imply endorsement or affiliation.