FDIC-Insured - Backed by the full faith and credit of the U.S. Government

-

-

-

Clint Sporhase

Vice President, Business Banking

Date Published: April 22, 2019

-

Important Financial Considerations to Consider When Setting Up Your Business

It's not uncommon for the subject of starting a business to come up when people discover I work in banking with small businesses. Folks are always keen to get my thoughts on their business ideas. I don’t pretend to be a definitive resource, but I do generally have a few things for prospective business owners to consider. A strong business plan is always the capstone to our conversation, but we’ll get to that in a minute. Here are a few other good common sense considerations.

Working for yourself

Working for yourself has some definite advantages, but it also comes with some challenges. Owning a business is not just an occupation, it is a lifestyle. Most folks focus on the potential financial upside. When it occurs, it is well deserved. Being able to “control your own destiny” in terms of money, time and business decisions is attractive. Each of those items also comes with a downside. Obviously, when a business struggles, the owners bear the brunt of the financial stress.

I also encourage prospective business owners to consider the time commitment. Things like covering for absent employees and all the other work that needs to occur outside normal business hours can take a toll on many people.

Viability of the business

Is your prospective business ready? Here are some questions to ask yourself:

- What need does the business fill? Understanding what value your business will bring to its customers and the market for it is critical in shaping your value proposition.

- Is the business differentiated? In many cases, I hear business owners say their customer service will set them apart. Keep in mind that service is an experience. It’s hard to use service as differentiator until you have a base of customers.

- Can you monetize the business and be profitable? Understanding what customers will pay for the good or service your business provides is another building block of success.

- Is it sustainable? Competition can undercut your prices and steal market share if your differentiator is easily duplicated.

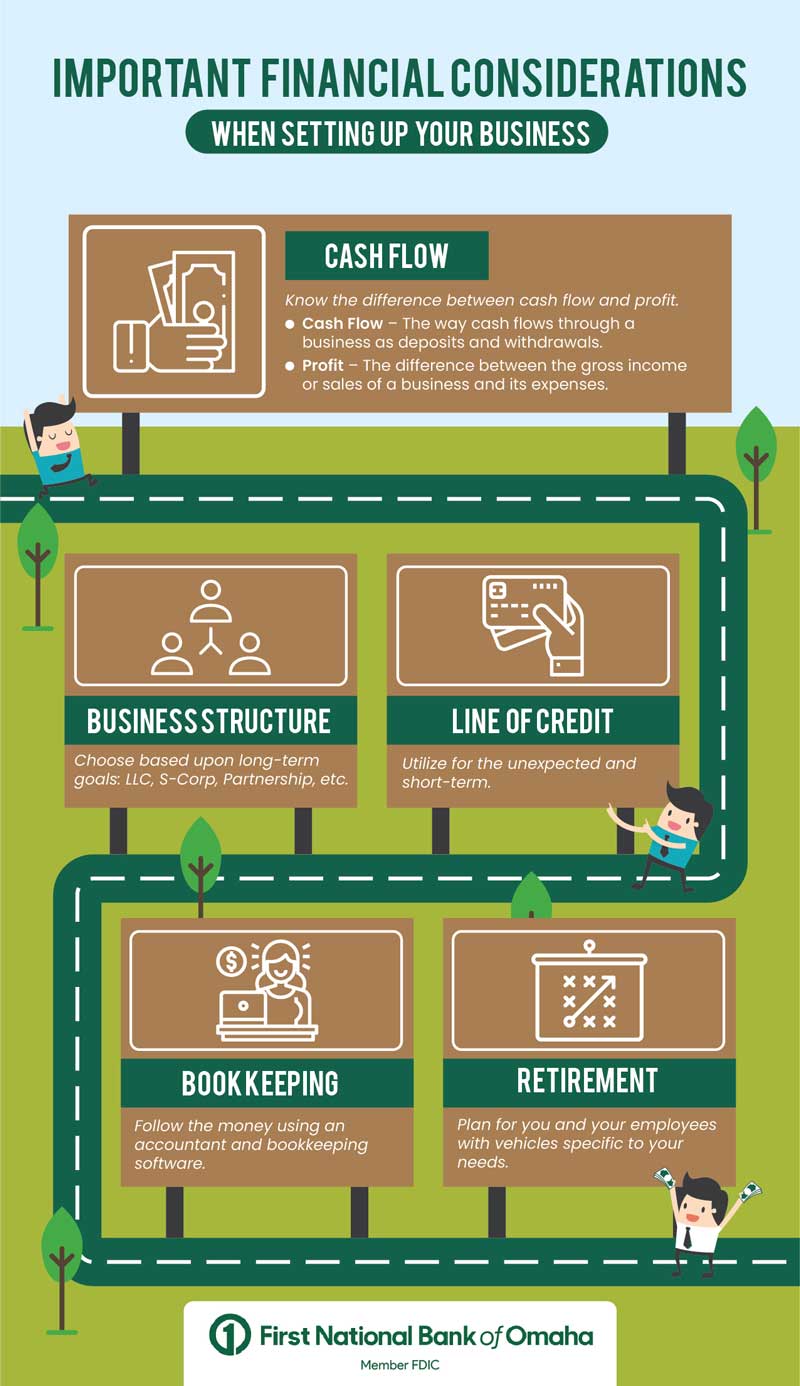

Money

Having a detailed understanding of how much money you will need to start your business and where it will come from is another critical consideration. Bankers call this the sources and uses of funding. Make sure your list of expenses is realistic. There are always surprises and delays in the startup process.

Thinking through where you plan to get the funding for your business is also critical. I encourage people to think of funding sources as a continuum. On one end, you have options like your own money and money from friends and family. While these may not always be an option, these sources are generally more open to risk. Your friends’ and family’s expectations for repayment and any potential return on their investments will vary. In the middle, you may have options like partners and investors. These two are generally more open to risk as well, but have a much higher return expectation – including ownership in the business. On the other end, you have options like Small Business Administration loans from your bank. These funds come with less tolerance for risk, but have a much lower return expectation in the form of interest.

Understanding the risk around your business idea will help you get a good idea what funding sources might make the most sense for your situation. Keep in mind the sources above are just some of the options out there. Each comes with costs and benefits.

The Plan

So, you‘ve made it this far and think your business idea has potential. Committing your idea and all the details around it to paper is next in the form of a business plan. Many times, I hear, “the bank or my investors are making me do a business plan.” Do the businesses plan for yourself first! If you can’t get comfortable with the plan, it is probably a good signal that you need to revisit your idea.

You can find lots of resources for business plans on the internet. The Small Business Administration website has a good template. (Following this template will also come in handy if a business loan ends up making sense in your situation.) Try to keep the plan as realistic as possible. I encourage people to look at some critical sections of the plan, like the financials, both as they expect things to happen and then again in a best/worst case scenario.

Finally, treat your plan as a living document and not as a one-time exercise. You will likely get some things right in your plan and some things wrong. Your success will likely hinge on your ability to correct errors and capitalize on successes.

If you are thinking about starting a business, good luck in your journey! If owning a business just isn’t for you, consider shopping at locally owned businesses to help keep our economy strong.

About the Author: Clint Sporhase leads First National Bank’s efforts to serve small business owners. Clint has 25 years of sales, marketing and strategy experience.

The articles in this blog are for informational purposes only and not intended to provide specific advice or recommendations. When making decisions about your financial situation, consult a financial professional for advice. Articles are not regularly updated, and information may become outdated.

-

Nearly 170 years of putting customers first.

-

-

Products

-

-

-

Company

-

-

-

Legal Information

-

© 2026 First National Bank of Omaha (FNBO). All Rights Reserved. 1601 Dodge Street, Omaha Nebraska, 68197

FNBO is an Equal Opportunity/Affirmative Action/Veterans/Disability Employer.

NMLS 412727

Cards are issued by FNBO (First National Bank of Omaha), pursuant to a license from Visa® U.S.A., Inc. Visa® is a registered trademark of Visa® International Service Association and used under license.

Only deposit products are FDIC insured.

Investment Products are: NOT FDIC INSURED • NOT A DEPOSIT OR OTHER OBLIGATION OF THE BANK • NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY • NOT GUARANTEED BY THE BANK • MAY LOSE VALUE

Awards based on independent surveys and editorial methodologies for the years shown. Recognition does not imply endorsement or affiliation.